Account opening fraud is escalating rapidly, with losses mounting for consumers and businesses alike. In fact, in its latest report, Solving Advanced Fraud in Account Opening, commissioned by Data Zoo, Liminal found that businesses lose an estimated $131,505 per successful fraud attack when taking into consideration indirect (such as case management), direct (monetary loss), and consumer loss (retention, drop-off) costs.

With new account fraud rising, it’s crucial to explore the challenges individuals and organizations face in identifying risks and vulnerabilities throughout the digital account opening process. To begin clamping down on fraud and stay ahead of fraudsters, we must first understand where current fraud-prevention solutions are falling short and the pain points they create for both businesses and consumers.

Current Solutions are Falling Short

The raw data on escalating fraud losses tells us that current account opening fraud-prevention platforms are falling short, but why is this? Faced with a wide range of use cases, account opening solutions must be equipped to prevent money-laundering, optimize customer onboarding, and prevent sophisticated fraud attacks. To simplify the vendor onboarding process, enterprises tend to seek out platforms that can solve multiple use cases.

However, building solutions to deal with such a broad array of challenges often leaves them stretched thin, with vulnerabilities to different types of fraud. The unintended consequence of focusing on use case-specific solutions is that, in many cases, vendors have stopped prioritizing the actual technical and data capabilities that lead to better fraud prevention. This misguided focus leads to significant pain points for both businesses and consumers.

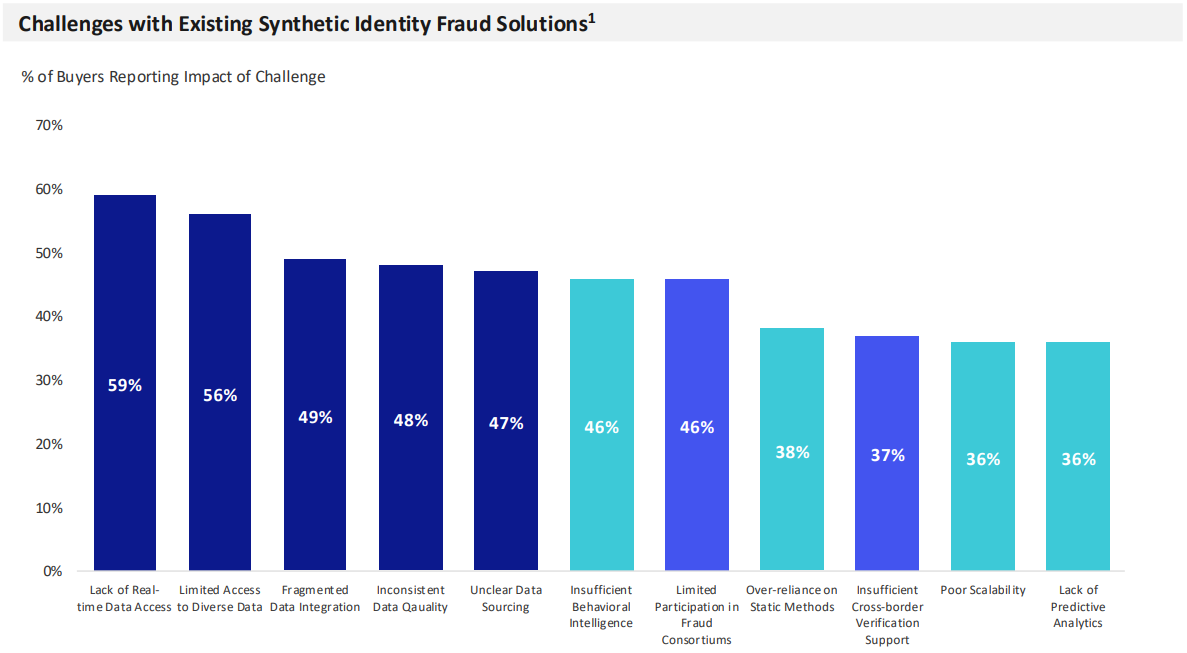

Account Opening Fraud Pain Points

The broad focus outlined above causes solutions to fail when it comes to solving account opening fraud, with many buyers reporting significant challenges in combating various types of fraud. The new Liminal report shows that 49% of buyers face challenges addressing synthetic identity fraud and 48% struggle with application fraud.

Enterprises surveyed in the report outlined several significant pain points with current solution providers that are hindering their ability to stop fraud:

Data Accessibility and Quality: Challenges with real-time access, data diversity, and integration create barriers to effective fraud prevention.

Analytical Capabilities: Weak analytics, static methods, and scalability issues limit the ability to detect and respond to fraud.

Network Limitations & Market Expertise: Gaps in fraud consortiums and cross-border verification reduce the effectiveness of collective defenses.

Lack of high-quality data stands out as a particular issue: more than half of the enterprises surveyed pointed to a lack of high-quality, real-time data as a key contributor to fraud. Furthermore, many businesses were unsure where and how their solution provider sourced their technical capabilities or verifiable data.

These gaps in existing solutions create opportunities for fraudsters to exploit. For many businesses, multiple vulnerabilities create a situation where they are constantly patching vulnerabilities in their systems, while being fully aware that other key issues exist.

Meeting the Challenge

Adopting more sophisticated fraud prevention solutions, particularly those that use high-quality data, is crucial for combating the rising threat of account opening fraud. Employing solutions that use a combination of authoritative data sources to create a more robust verification process can remove data-related pain points and significantly improve the chances of identifying fraud before an account can be created.

Data Zoo’s layered approach to identity verification increases certainty that businesses are addressing the evolving nature of identity fraud, using authoritative data for processes including:

Document Fraud: Data Zoo’s authoritative data allows you to cross-reference the information on a document (name, address, date of birth, etc.) with trusted sources like government databases or credit bureaus. This helps identify discrepancies that might indicate a forged document.

Synthetic Identity Fraud: Synthetic identities are created by combining real and fake information. Fraudsters might use a real Social Security number but pair it with a fabricated name and address. Authoritative data from Data Zoo helps expose these inconsistencies.

Data Depth & Breadth With Unique Sequencing Approach: Data Zoo offers an ever-growing catalogue of data assets encompassing integrations with more than 150 sources, optimizing match rates, response times, and transaction costs.

The shortcomings of current fraud-prevention solutions cause numerous pain points for consumers and businesses alike. Employing tools with robust, authoritative data sources can go a long way in removing these pain points and combating fraud.

Be sure to keep following as we continue to explore account opening fraud in a blog series leading up to the release of Liminal’s latest report, Solving Advanced Fraud in Account Opening, commissioned by Data Zoo. The first blog in the series, covering the rise in account opening fraud, can be found here.